Introduction : An overview of the background

- Labour falls under the Concurrent List of the Constitution. Therefore, both Parliament and state legislatures can make laws regulating labour.

- Central Government stated that there are over 100 state and 40 central laws regulating various aspects of labour such as resolution of industrial disputes, working conditions, social security and wages. The Second National Commission on Labour (2002) found existing laws to be complex, with archaic provisions and inconsistent definitions.

- To improve ease of compliance and ensure uniformity in labour laws, the Central Government recommended the consolidation of central labour laws into broader groups such as:

- industrial relations,

- wages,

- social security,

- safety, and

- welfare and working conditions.

- In 2019, the Ministry of Labour and Employment introduced 4 Bills to consolidate 29 central laws. These Codes regulate: (i) Wages, (ii) Industrial Relations, (iii) Social Security, and (iv) Occupational Safety, Health and Working Conditions.

Introduction : Journey of the bill so far

The Code On Social Security, 2020 was introduced in the Lok Sabha on 19th September 2020. Journey of the Bill so far:

With this notification the Code of Social Security and the other labour codes stands implemented. Further, rules under the Codes are expected to be notified within the next 45 days.

Refer following article :

https ://labour.gov.in/sites/default/files/pib2192463.pdf

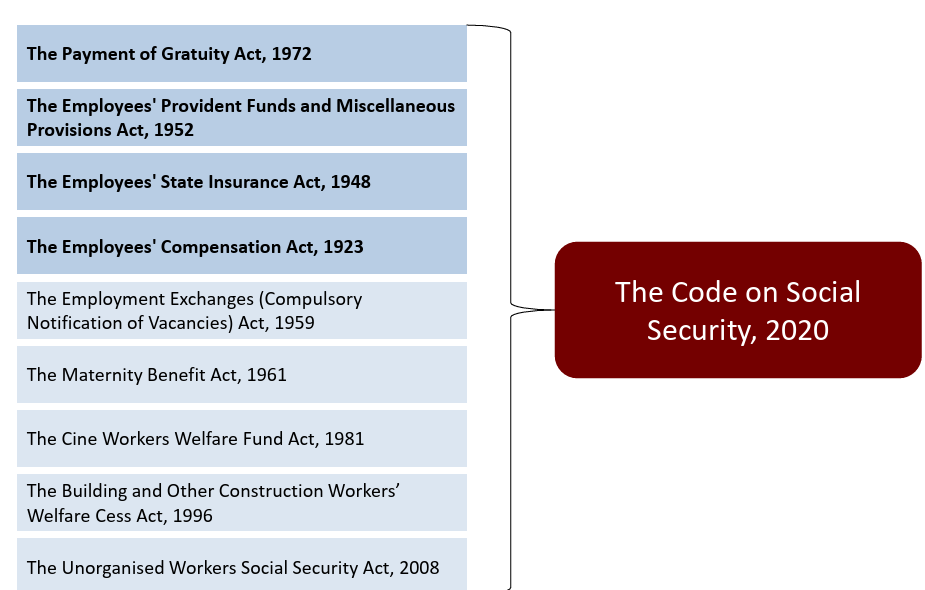

Introduction : Acts merging into the Code on Social Security, 2020

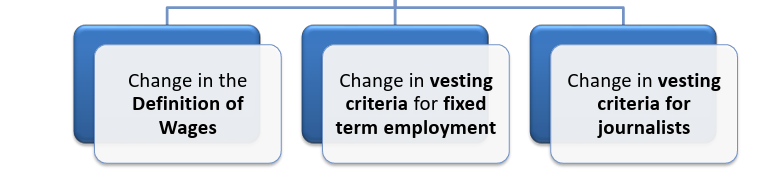

Key changes

Note: Above are the key changes only and there may be other changes as well. We are not lawyers and it is best to consult a labour law consultant to get a complete overview of the changes you need to implement for your organization.

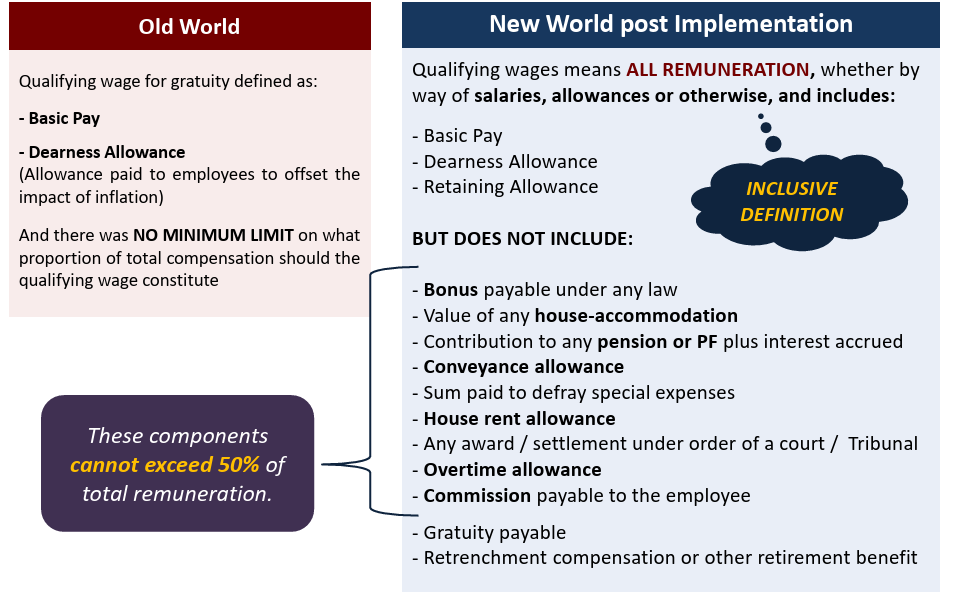

Definition of Wages : What does Section 2 Sub Section 88 require?

Text of subsection 88:

(88) “wages” means all remuneration, whether by way of salaries, allowances or otherwise, expressed in terms of money or capable of being so expressed which would, if the terms of employment, express or implied, were fulfilled, be payable to a person employed in respect of his employment or of work done in such employment, and includes,—

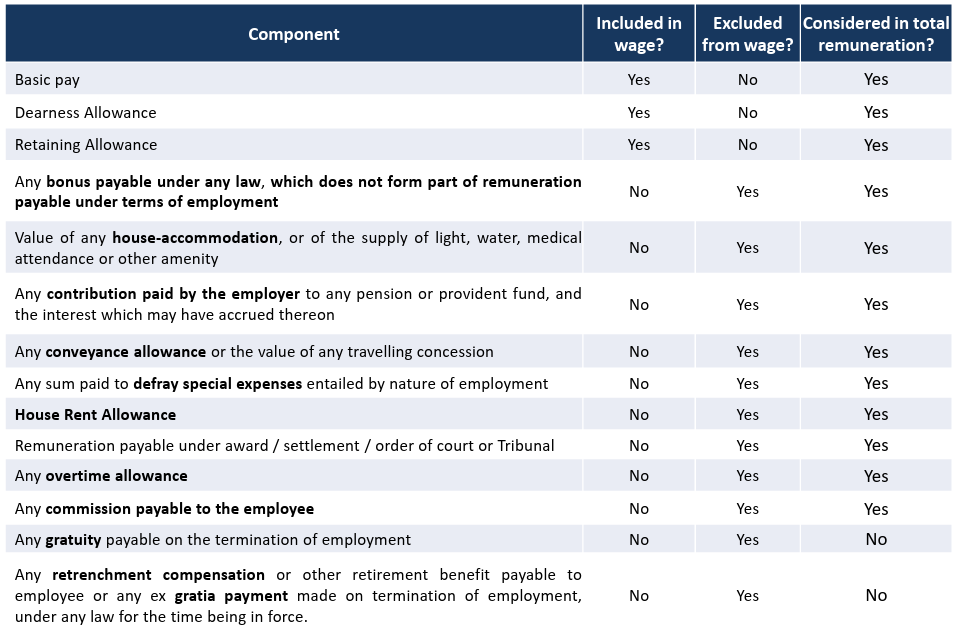

(a) basic pay;

(b) dearness allowance; and

(c) retaining allowance, if any,

but does not include—

(a) any bonus payable under any law for the time being in force, which does not form part of the remuneration payable under the terms of employment;

(b) the value of any house-accommodation, or of the supply of light, water, medical attendance or other amenity or of any service excluded from the computation of wages by a general or special order of the appropriate Government;

(c) any contribution paid by the employer to any pension or provident fund, and the interest which may have accrued thereon;

(d) any conveyance allowance or the value of any travelling concession;

(e) any sum paid to the employed person to defray special expenses entailed on him by the nature of his employment;

(f) house rent allowance;

(g) remuneration payable under any award or settlement between the parties or order of a court or Tribunal; (h) any overtime allowance;

(i) any commission payable to the employee;

(j) any gratuity payable on the termination of employment;

(k) any retrenchment compensation or other retirement benefit payable to the employee or any ex gratia payment made to him on the termination of employment, under any law for the time being in force:

Provided that for calculating the wages under this clause, if payments made by the employer to the employee under sub-clauses (a) to (i) exceeds one half, or such other per cent. as may be notified by the Central Government, of the all remuneration calculated under this clause, the amount which exceeds such one-half, or the per cent. so notified, shall be deemed as remuneration and shall be accordingly added in wages under this clause.

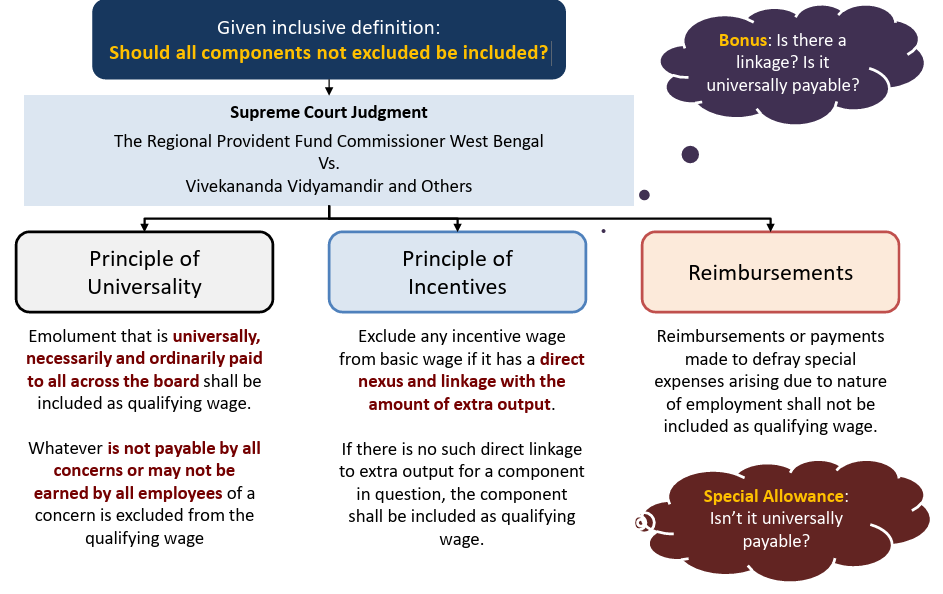

Key Question : Which components should be included in wage?

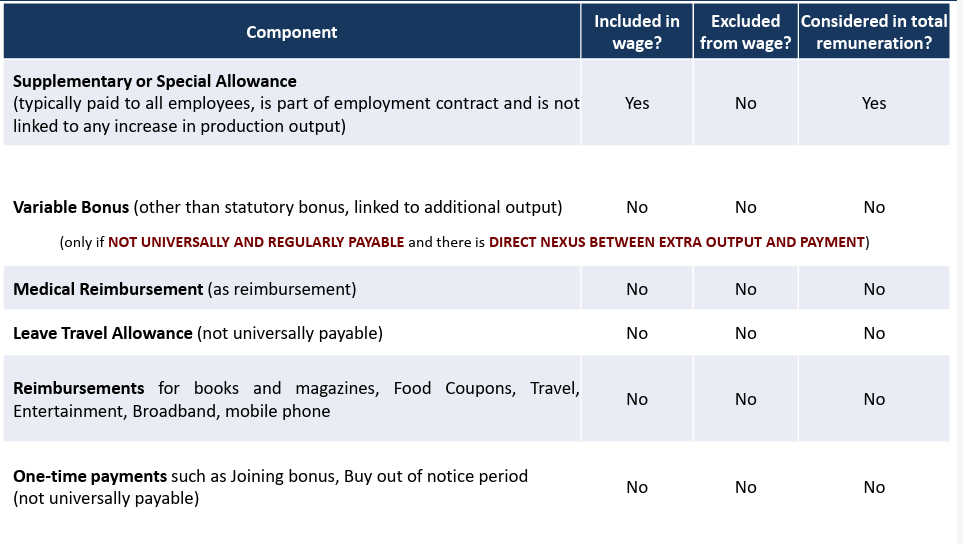

Common components of Salary : Components LISTED in the definition

Common components of Salary : Components NOT LISTED in the definition

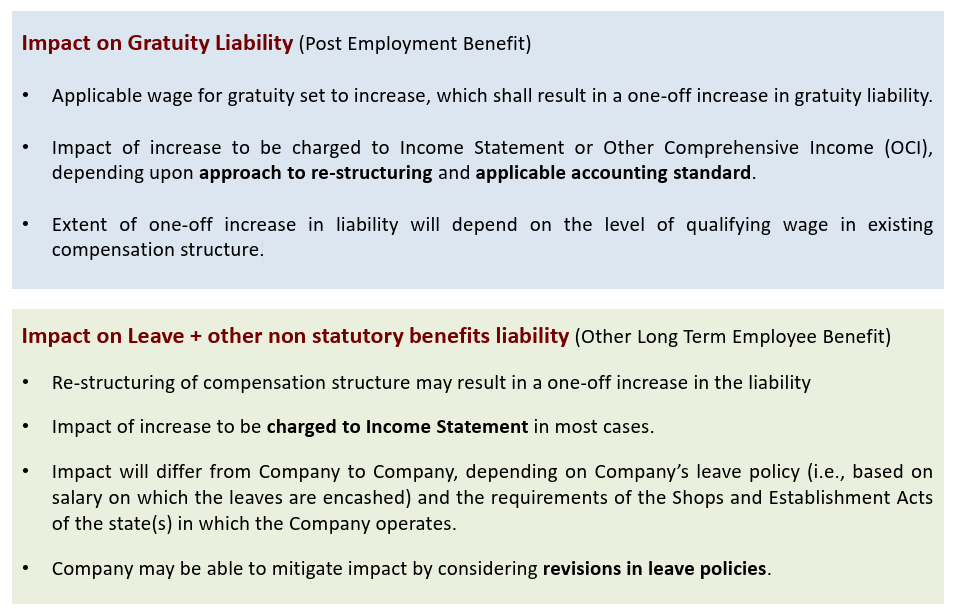

Definition of Wages : Implication of the Change

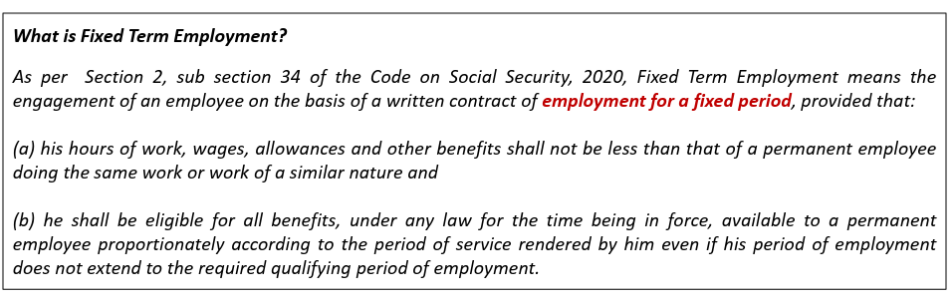

Fixed Term Employment : Vesting Criteria to not apply

In case of Fixed Term Employment, gratuity pay-outs will be made upon expiry of the fixed term, irrespective of whether an year has been completed or not. This is expected to result in increase in gratuity liability in case of Companies that offer fixed term employment. The increase in liability because of this change shall be treated as Past Service Cost and charged to Income Statement, either immediately or over a period (depending upon the applicable accounting standard).

Disclaimers:

This presentation and any accompanying material or talk, if any, has been furnished / made available to you solely for your information and must not be reproduced or redistributed. This material is for the information of the recipient and we are not soliciting any action based upon it.

Also, it does not constitute any recommendation. It should also be noted that we are not engaged in the practice of law. The information contained in this document does not constitute and is not a substitute for legal advice. The Company should consult a labour law consultant / lawyer for any legal advice relating to the implementation of the Code on Social Security, 2020.